#Computer Numerical Control Market Share

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr was the first site to host the blog for President Barack Obama in 2011.

Text

#Computer Numerical Control Market#Computer Numerical Control Market Share#Computer Numerical Control Market Size#Computer Numerical Control Market Research#Computer Numerical Control Industry#What is Computer Numerical Control?

0 notes

Text

CNC development history and processing principles

CNC machine tools are also called Computerized Numerical Control (CNC for short). They are mechatronics products that use digital information to control machine tools. They record the relative position between the tool and the workpiece, the start and stop of the machine tool, the spindle speed change, the workpiece loosening and clamping, the tool selection, the start and stop of the cooling pump and other operations and sequence actions on the control medium with digital codes, and then send the digital information to the CNC device or computer, which will decode and calculate, issue instructions to control the machine tool servo system or other actuators, so that the machine tool can process the required workpiece.

1. The evolution of CNC technology: from mechanical gears to digital codes

The Beginning of Mechanical Control (late 19th century - 1940s)

The prototype of CNC technology can be traced back to the invention of mechanical automatic machine tools in the 19th century. In 1887, the cam-controlled lathe invented by American engineer Herman realized "programmed" processing for the first time by rotating cams to drive tool movement. Although this mechanical programming method is inefficient, it provides a key idea for subsequent CNC technology. During World War II, the surge in demand for military equipment accelerated the innovation of processing technology, but the processing capacity of traditional machine tools for complex parts had reached a bottleneck.

The electronic revolution (1950s-1970s)

After World War II, manufacturing industries mostly relied on manual operations. After workers understood the drawings, they manually operated machine tools to process parts. This way of producing products was costly, inefficient, and the quality was not guaranteed. In 1952, John Parsons' team at the Massachusetts Institute of Technology (MIT) developed the world's first CNC milling machine, which input instructions through punched paper tape, marking the official birth of CNC technology. The core breakthrough of this stage was "digital signals replacing mechanical transmission" - servo motors replaced gears and connecting rods, and code instructions replaced manual adjustments. In the 1960s, the popularity of integrated circuits reduced the size and cost of CNC systems. Japanese companies such as Fanuc launched commercial CNC equipment, and the automotive and aviation industries took the lead in introducing CNC production lines.

Integration of computer technology (1980s-2000s)

With the maturity of microprocessor and graphical interface technology, CNC entered the PC control era. In 1982, Siemens of Germany launched the first microprocessor-based CNC system Sinumerik 800, whose programming efficiency was 100 times higher than that of paper tape. The integration of CAD (computer-aided design) and CAM (computer-aided manufacturing) software allows engineers to directly convert 3D models into machining codes, and the machining accuracy of complex surfaces reaches the micron level. During this period, equipment such as five-axis linkage machining centers came into being, promoting the rapid development of mold manufacturing and medical device industries.

Intelligence and networking (21st century to present)

The Internet of Things and artificial intelligence technologies have given CNC machine tools new vitality. Modern CNC systems use sensors to monitor parameters such as cutting force and temperature in real time, and use machine learning to optimize processing paths. For example, the iSMART Factory solution of Japan's Mazak Company achieves intelligent scheduling of hundreds of machine tools through cloud collaboration. In 2023, the global CNC machine tool market size has exceeded US$80 billion, and China has become the largest manufacturing country with a production share of 31%.

2. CNC machining principles: How code drives steel

The essence of CNC technology is to convert the physical machining process into a control closed loop of digital signals. Its operation logic can be divided into three stages:

Geometric Modeling and Programming

After building a 3D model using CAD software such as UG and SolidWorks, CAM software “deconstructs” the model: automatically calculating parameters such as tool path, feed rate, spindle speed, and generating G code (such as G01 X100 Y200 F500 for linear interpolation to coordinates (100,200) and feed rate 500mm/min). Modern software can even simulate the material removal process and predict machining errors.

Numerical control system analysis and implementation

The "brain" of CNC machine tools - the numerical control system (such as Fanuc 30i, Siemens 840D) converts G codes into electrical pulse signals. Taking a three-axis milling machine as an example, the servo motors of the X/Y/Z axes receive pulse commands and convert rotary motion into linear displacement through ball screws, with a positioning accuracy of up to ±0.002mm. The closed-loop control system uses a grating ruler to feedback position errors in real time, forming a dynamic correction mechanism.

Multi-physics collaborative control

During the machining process, the machine tool needs to coordinate multiple parameters synchronously: the spindle motor drives the tool to rotate at a high speed of 20,000 rpm, the cooling system sprays atomized cutting fluid to reduce the temperature, and the tool changing robot completes the tool change within 0.5 seconds. For example, when machining titanium alloy blades, the system needs to dynamically adjust the cutting depth according to the hardness of the material to avoid tool chipping.

3. The future of CNC technology: cross-dimensional breakthroughs and industrial transformation

Currently, CNC technology is facing three major trends:

Combined: Turning and milling machine tools can complete turning, milling, grinding and other processes on one device, reducing clamping time by 90%;

Additive-subtractive integration: Germany's DMG MORI's LASERTEC series machine tools combine 3D printing and CNC finishing to directly manufacture aerospace engine combustion chambers;

Digital Twin: By using a virtual machine tool to simulate the actual machining process, China's Shenyang Machine Tool's i5 system has increased debugging efficiency by 70%.

From the meshing of mechanical gears to the flow of digital signals, CNC technology has rewritten the underlying logic of the manufacturing industry in 70 years. It is not only an upgrade of machine tools, but also a leap in the ability of humans to transform abstract thinking into physical entities. In the new track of intelligent manufacturing, CNC technology will continue to break through the limits of materials, precision and efficiency, and write a new chapter for industrial civilization.

#prototype machining#cnc machining#precision machining#prototyping#rapid prototyping#machining parts

2 notes

·

View notes

Text

How to Choose the Best ERP for Engineering and Manufacturing Industry

In today’s fast-paced world, engineering and manufacturing companies face increasing pressure to deliver high-quality products while maintaining efficiency and cost-effectiveness. Implementing the right Enterprise Resource Planning (ERP) software can significantly enhance operations, streamline workflows, and boost productivity. However, with numerous options available, selecting the best ERP software for the engineering and manufacturing industry can be challenging. This guide will help you navigate this decision-making process and choose the most suitable solution for your business.

Why ERP is Crucial for Engineering and Manufacturing

ERP software integrates various business processes, including production, inventory management, supply chain, finance, and human resources. For engineering and manufacturing companies, ERP solutions are particularly vital because they:

Facilitate real-time data sharing across departments.

Enhance supply chain management.

Optimize production planning and scheduling.

Ensure compliance with industry standards.

Reduce operational costs.

Partnering with the right Engineering ERP software company ensures that your organization leverages these benefits to stay competitive in a dynamic market.

Steps to Choose the Best ERP for Engineering and Manufacturing

1. Understand Your Business Needs

Before exploring ERP solutions, evaluate your company’s specific requirements. Identify the pain points in your current processes and prioritize the features you need in an ERP system. Common features for engineering and manufacturing companies include:

Bill of Materials (BOM) management

Production planning and scheduling

Inventory control

Quality management

Financial reporting

Consulting with a reputed ERP software company can help you match your needs with the right features.

2. Look for Industry-Specific Solutions

Generic ERP software might not address the unique needs of the engineering and manufacturing sector. Opt for an ERP software in India that offers modules tailored to your industry. Such solutions are designed to handle specific challenges like multi-level BOM, project costing, and shop floor management.

3. Check Vendor Expertise

Choosing a reliable vendor is as important as selecting the software itself. Research ERP solution providers with a strong track record in serving engineering and manufacturing companies. Look for reviews, case studies, and client testimonials to gauge their expertise.

4. Evaluate Scalability and Flexibility

Your business will grow, and so will your operational requirements. Ensure that the ERP system you choose is scalable and flexible enough to accommodate future needs. The top 10 ERP software providers in India offer scalable solutions that can adapt to changing business demands.

5. Assess Integration Capabilities

An ERP system must integrate seamlessly with your existing tools, such as Computer-Aided Design (CAD) software, Customer Relationship Management (CRM) systems, and IoT devices. A well-integrated system reduces redundancies and enhances efficiency.

6. Prioritize User-Friendliness

A complex system with a steep learning curve can hinder adoption. Choose an ERP software with an intuitive interface and easy navigation. This ensures that your employees can use the system effectively without extensive training.

7. Consider Customization Options

No two businesses are alike. While standard ERP solutions offer core functionalities, some companies require customization to align with specific workflows. A trusted ERP software company in India can provide custom modules tailored to your unique needs.

8. Focus on Data Security

Engineering and manufacturing companies often deal with sensitive data. Ensure that the ERP solution complies with the latest security standards and offers robust data protection features.

9. Compare Pricing and ROI

While cost is an important factor, it should not be the sole criterion. Evaluate the long-term return on investment (ROI) offered by different ERP software. A slightly expensive but feature-rich solution from the best ERP software provider in India may deliver better value than a cheaper alternative with limited functionalities.

10. Test Before You Commit

Most ERP software companies offer free trials or demo versions. Use these opportunities to test the software in a real-world scenario. Gather feedback from your team and ensure the solution meets your expectations before finalizing your decision.

Benefits of Partnering with the Best ERP Software Providers in India

India is home to some of the leading ERP software providers in India, offering state-of-the-art solutions for the engineering and manufacturing sector. Partnering with a reputable provider ensures:

Access to advanced features tailored to your industry.

Reliable customer support.

Comprehensive training and implementation services.

Regular updates and enhancements to the software.

Companies like Shantitechnology (STERP) specialize in delivering cutting-edge ERP solutions that cater specifically to engineering and manufacturing businesses. With years of expertise, they rank among the top 10 ERP software providers in India, ensuring seamless integration and exceptional performance.

Conclusion

Selecting the right ERP software is a critical decision that can impact your company’s efficiency, productivity, and profitability. By understanding your requirements, researching vendors, and prioritizing features like scalability, integration, and security, you can find the perfect ERP solution for your engineering or manufacturing business.

If you are looking for a trusted ERP software company in India, consider partnering with a provider like STERP. As one of the best ERP software providers in India, STERP offers comprehensive solutions tailored to the unique needs of engineering and manufacturing companies. With their expertise, you can streamline your operations, improve decision-making, and stay ahead in a competitive market.

Get in touch with STERP – the leading Engineering ERP software company – to transform your business with a reliable and efficient ERP system. Take the first step toward a smarter, more connected future today!

#Manufacturing ERP software company#ERP solution provider#Engineering ERP software company#ERP software company#ERP software companies

6 notes

·

View notes

Text

Risks and Rewards: Navigating the Evolving Speech-to-Text API Market

Speech-to-text API Market Growth & Trends

The global speech-to-text API market is experiencing robust growth, projected to reach USD 8,569.5 million by 2030, growing at a CAGR of 14.1% from 2025 to 2030. This expansion is driven by several key factors:

Rising Popularity of Smart Speakers and Smart Mobile Phones:

The widespread adoption of voice-enabled systems in smart speakers and mobile phones is a significant driver. These devices leverage augmented reality (AR), machine learning (ML), and natural language processing (NLP) to automate conversations and provide a hands-free user experience. As more consumers integrate these devices into their daily routines, the demand for underlying speech-to-text API solutions continues to surge.

Increasing Demand for Transcription and Real-time Support Services:

The growing need for accurate transcription and real-time support services across various industries is motivating industry giants to develop advanced speech-to-text API solutions. This includes applications in contact centers, legal documentation, content creation, and more, where converting spoken words into text efficiently is crucial.

Growth in Virtual/Digital Conferences and Events:

The increasing number of virtual and digital conferences and events hosted by technology giants and other enterprises is boosting the demand for speech-to-text solutions. These solutions offer low cost, high accuracy, and faster transcription, enabling seamless communication and accessibility for a global audience. For instance, events like PegaWorldiNspire utilize AI technologies, including speech-to-text, to enhance the viewer experience.

Advancements in Artificial Intelligence (AI) and Cloud-based Services:

Significant advancements in AI, particularly in machine learning and natural language processing, are enhancing the accuracy and capabilities of speech-to-text APIs. The rising popularity of cloud-based services also facilitates the adoption of these solutions by offering scalability, cost-efficiency, and remote accessibility.

Enhanced Accessibility for People with Disabilities:

Speech-to-text solutions play a vital role in improving accessibility for individuals with disabilities. They allow people with visual impairments to "hear" written words when combined with screen readers and provide voice control for individuals with motor impairments. Companies like Voiceitt are specifically developing speech recognition for non-standard speech, opening up voice technology for people with speech disabilities.

Continuous Product Improvement and Innovation:

Companies in the market are actively improving their product ranges by integrating advanced technologies. For example, Google LLC launched a new model for its Speech-to-Text API in April 2022, improving accuracy across numerous languages and supporting diverse acoustic and environmental conditions. Similarly, IBM Corporation upgraded its speech-to-text recognition service in March 2020, enhancing tracking capabilities and adding speaker labels for Korean and German language models. Other key players like Amazon Transcribe, Microsoft Azure Speech Service, Nuance (Dragon Speech Recognition), Deepgram, and AssemblyAI are continuously innovating to offer higher accuracy, multilingual support, and industry-specific solutions.

Curious about the Speech-to-text API Market? Download your FREE sample copy now and get a sneak peek into the latest insights and trends.

Speech-to-text API Market Report Highlights

Software component led the market with a revenue share of 70.3% in 2024. High penetration of software segment can be attributed to advancements in increased computing power, information storage capacity, and parallel processing capabilities to supply high-end services.

The on-premises segment dominates the market with a revenue share in 2024. The on-premises deployment model is preferred by sectors related to communication, marketing, HR, legal departments, studios, researchers, and broadcasters, among others, due to security concerns.

The large enterprise segment dominates the market, with a revenue share in 2024. The major factor propelling the growth of the segment is the high capital stability, which allows large enterprises to afford such APIs integrations.

The fraud detection & prevention segment dominates the market with a revenue share in 2024. This is due to the growing need for speech-to-text APIs in the entertainment and media industry.

The BFSI segment dominates the market, with a revenue share in 2024. The major factor propelling segment growth is using speech-to-text converters to analyze the customer’s feedback.

Speech-to-text API Market Segmentation

Grand View Research has segmented the global Speech-to-text API market based on components, deployment, organization size, application, verticals, and region:

Speech-to-text API Component Outlook (Revenue, USD Million, 2018 - 2030)

Software

Service

Speech-to-text API Deployment Outlook (Revenue, USD Million, 2018 - 2030)

On-premises

Cloud

Speech-to-text API Organization size Outlook (Revenue, USD Million, 2018 - 2030)

Large Enterprises

Small & Medium-sized Enterprises (SMEs)

Speech-to-text API Application Outlook (Revenue, USD Million, 2018 - 2030)

Contact center and customer management

Content Transcription

Fraud Detection and Prevention

Risk and Compliance Management

Subtitle Generation

Others

Speech-to-text API Verticals Outlook (Revenue, USD Million, 2018 - 2030)

BFSI

IT & Telecom

Healthcare

Retail & eCommerce

Government & Defense

Media & Entertainment

Travel & Hospitality

Others

Download your FREE sample PDF copy of the Speech-to-text API Market today and explore key data and trends.

0 notes

Text

Global AI Camera Market Set for Exponential Growth Through 2034

The global Artificial Intelligence (AI) camera market was valued at approximately US$ 7.8 billion in 2023 and is projected to grow exponentially, reaching US$ 35.5 billion by 2034. Driven by rapid advances in machine learning, edge computing, and data analytics, AI cameras have evolved far beyond basic image capturing tools. They now offer sophisticated features such as facial recognition, behavior analysis, motion detection, and anomaly detection, making them indispensable across multiple industries including security, retail, transportation, healthcare, and smart city applications.

AI cameras enable real-time data processing and seamless integration with Internet of Things (IoT) ecosystems, further enhancing automation and live monitoring capabilities. This growing demand for intelligent, automated, and responsive camera systems is the core driver of the market's robust growth trajectory.

Market Drivers & Trends

The AI camera market is propelled by several critical factors:

Growing Demand for Advanced Surveillance Solutions: Rising security concerns in residential, commercial, and public spaces have accelerated adoption of AI-powered surveillance systems capable of advanced tasks like facial recognition and real-time threat detection.

Increased Focus on Data Analytics and Business Intelligence: AI cameras extract actionable insights from visual data, optimizing operational efficiencies and supporting predictive maintenance, especially in industries such as transportation and retail.

Advancements in Consumer Electronics: Smartphones and other consumer devices increasingly incorporate AI cameras, offering features like scene recognition, object detection, and AI-enhanced photography.

For example, Eufy's Indoor Cam E30 combines 4K video recording with AI-driven human and pet detection at an affordable price point. Meanwhile, Verkada showcases AI-driven alerts integrated with cloud-based security platforms.

Latest Market Trends

Hybrid Deployment Leading the Market: Hybrid AI camera systems, combining indoor and outdoor coverage with centralized monitoring, accounted for over 85% market share in 2023. Their versatility makes them popular in both residential and commercial applications.

Smartphone AI Cameras Driving Consumer Demand: Smartphones remain the largest segment, as users expect AI features such as facial identification and automatic camera setting adjustments.

Edge AI Processing: Collaborations like Sony Semiconductor Solutions and Raspberry Pi’s development of an edge AI board enable processing visual data on-device, reducing latency and increasing privacy.

Key Players and Industry Leaders

The AI camera market landscape is moderately fragmented with numerous prominent players expanding product portfolios and pursuing mergers and acquisitions to strengthen market presence. Leading companies include:

AV Costar

Axis Communications AB

Bosch Sicherheitssysteme GmbH

Canon Inc.

Dahua Technology

Hangzhou Hikvision Digital Technology Co., Ltd.

Honeywell International Inc.

Huawei Technologies Co., Ltd.

Huddly Inc.

Johnson Controls

LG Electronics

Nikon Corporation

Panasonic Holdings Corporation

Samsung Electronics Co., Ltd.

Sony Corporation

Teledyne FLIR LLC

Vivotek, Inc.

Each continues to invest heavily in R&D, aiming to introduce innovative AI-powered camera systems across various market segments.

Recent Developments

In September 2024, Panasonic launched the AI corner camera i-PRO Corner Camera, designed specifically for high-security environments such as prisons and rehabilitation centers. It features a 5-megapixel sensor, wide-angle view, and invisible IR-LED for low-light clarity.

In February 2024, Canon unveiled the EOS R5 Mark II, its first AI-powered camera featuring a 45MP sensor and Deep Learning AF autofocus, which uses trained algorithms to recognize subjects for superior focusing performance.

Gain a preview of important insights from our Report in this sample – https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=86009

Market Opportunities

The AI camera market offers multiple growth opportunities:

Smart Cities: Urban centers worldwide are increasingly implementing AI cameras for traffic management, public safety, and infrastructure monitoring.

Retail Analytics: AI cameras facilitate people counting, customer behavior analysis, and occupancy detection, enabling retailers to optimize store layouts and improve customer experiences.

Automotive and Smart Homes: Growing integration of AI cameras in vehicles and smart home security solutions opens new avenues for innovation and adoption.

Emerging Markets: Asia Pacific, driven by countries like China, Japan, and India, shows high potential due to large consumer bases and government investments in AI research.

Future Outlook

Analysts project sustained growth for the AI camera market, driven by continuous technological innovation and rising adoption across diverse sectors. By 2034, the market is expected to quintuple in value from 2023, supported by enhanced AI capabilities such as:

Improved edge computing reducing reliance on cloud infrastructure

Advanced analytics for predictive and proactive security measures

Increasing consumer preference for smart and automated systems

The convergence of AI cameras with IoT and 5G connectivity will further accelerate adoption, making AI cameras a cornerstone of next-generation intelligent surveillance and monitoring ecosystems.

Market Segmentation

The AI camera market is segmented by product type, resolution, deployment, application, and end-user:

By Product Type: Compact cameras, DSLR cameras, consumer electronics/smartphone cameras, CCTV cameras (including dome, bullet, turret, fisheye, PTZ), and others (miniature, panoramic).

By Resolution: Up to 2MP, 3MP-6MP, 7MP-10MP, 11MP-15MP, and above 15MP.

By Deployment: Indoor, outdoor, hybrid.

By Application: Intrusion detection, smart farming, automated sports broadcasting, people counting, license plate detection, face detection, occupancy detection, and others (fall detection, hard hat detection).

By End-User: Residential/individual, commercial (office buildings, retail stores, airports/railways, highways, hotels/restaurants), and industrial sectors.

Regional Insights

Asia Pacific leads the market with contributions of approximately US$ 2.9 billion in 2023, driven by rapid adoption in China, Japan, India, and ASEAN countries. Investments in AI R&D and large-scale deployment of smart devices fuel growth.

North America holds a significant 31.5% market share, benefiting from mature infrastructure, early adoption, and stringent security regulations.

Europe offers a stable market with emphasis on privacy and data protection, encouraging responsible AI camera usage.

Other regions like the Middle East & Africa and Latin America are gradually increasing their footprint in the AI camera space.

Why Buy This Report?

This comprehensive AI camera market report offers:

Detailed quantitative and qualitative analysis including market size, growth forecasts, and trends through 2034.

In-depth competitive landscape and company profiles covering product portfolios, strategies, and recent developments.

Market segmentation insights to identify key opportunities and industry dynamics.

Regional and country-level analysis enabling strategic market entry or expansion.

Expert viewpoints and future outlook helping stakeholders make informed decisions.

Frequently Asked Questions

Q1. What is driving the rapid growth of the AI camera market? A1. The integration of AI with camera technologies, increased demand for advanced surveillance, and growth in consumer electronics featuring AI cameras are key growth drivers.

Q2. Which regions offer the highest growth potential? A2. Asia Pacific leads in growth potential due to massive consumer bases and government investments, followed by North America and Europe.

Q3. What are the major applications of AI cameras? A3. Security and surveillance, retail analytics, smart city infrastructure, automotive systems, and consumer electronics are prominent applications.

Q4. Who are the key players in the AI camera market? A4. Leading companies include Canon, Panasonic, Hikvision, Sony, Samsung, Bosch, Honeywell, and others.

Q5. What trends should businesses watch? A5. Hybrid deployment systems, edge AI processing, smartphone AI cameras, and IoT integration are key trends shaping the future of AI cameras.

About Transparency Market Research Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information. Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports. Contact: Transparency Market Research Inc. CORPORATE HEADQUARTER DOWNTOWN, 1000 N. West Street, Suite 1200, Wilmington, Delaware 19801 USA Tel: +1-518-618-1030 USA - Canada Toll Free: 866-552-3453 Website: https://www.transparencymarketresearch.com Email: [email protected]

0 notes

Text

How Indian CNC Machine Companies Stay Affordable

India has steadily emerged as a global manufacturing hub, and the CNC (Computer Numerical Control) machine industry is no exception. Indian CNC machine companies have built a reputation for delivering high-quality machines at competitive prices, making them a go-to choice for many manufacturers around the world. But how exactly do these companies manage to stay affordable without compromising on quality? The answer lies in a combination of smart manufacturing practices, efficient resource management, and an understanding of market dynamics.

1. Localized Manufacturing and Sourcing

One of the key reasons Indian CNC machine companies can offer affordability is their strong reliance on local manufacturing and sourcing. By using locally available raw materials, components, and labor, they eliminate the high costs associated with imports and international logistics. This also enables faster turnaround times and better quality control, as the supply chain is shorter and more manageable.

Furthermore, India’s rich base of engineering talent and raw material availability, especially in steel and alloys, ensures that costs remain lower compared to Western markets. This strategic localization directly translates into reduced production costs.

2. Lean Manufacturing Practices

CNC machine manufacturers Indian often implement lean manufacturing practices to minimize waste and maximize efficiency. These practices include just-in-time inventory systems, modular design approaches, and continuous process improvements. By streamlining operations and reducing overheads, these companies can keep production costs low.

Additionally, many Indian companies use in-house machining for key parts rather than outsourcing. This not only ensures better control over quality and lead times but also reduces dependency on expensive third-party suppliers.

3. Cost-Effective Labor Force

India’s large pool of skilled and semi-skilled labor is a significant advantage. While the quality of work remains high due to rigorous training and vocational programs, labor costs in India are considerably lower than in developed countries. This allows Indian CNC manufacturers to invest more in R&D, automation, and product enhancement while still keeping final machine prices affordable.

Moreover, the presence of industrial clusters, such as those in Rajkot, Pune, Coimbatore, and Bengaluru, fosters an ecosystem where businesses can tap into a shared pool of resources, talent, and infrastructure, further reducing operational costs.

4. Focus on Standardization and Scalability

To keep prices competitive, Indian CNC companies often focus on standard machine models that can be easily scaled and modified. By standardizing key components and modules, manufacturers achieve economies of scale. Producing machines in batches reduces per-unit costs and makes it easier to manage inventory.

At the same time, these machines are built with scalability in mind. Customers can start with a basic model and upgrade it as needed. This modular approach allows businesses to invest according to their immediate needs, which increases the appeal of Indian CNC machines in cost-sensitive markets.

5. Government Support and Export Incentives

The Indian government has played a supportive role in boosting domestic manufacturing through initiatives like “Make in India” and various MSME (Micro, Small and Medium Enterprises) development programs. CNC manufacturers often benefit from subsidies, tax incentives, and easier access to credit, helping them maintain competitive pricing.

Additionally, many Indian companies receive export incentives that make it easier to tap into global markets. These incentives reduce the cost burden on exporters and make their products more attractive internationally.

6. Customer-Centric After-Sales Service

While affordability is key, Indian CNC machine companies also emphasize strong after-sales service and customer support. By offering reliable service, easy availability of spare parts, and remote troubleshooting options, they reduce the total cost of ownership for the customer. This holistic value proposition — affordable purchase and low maintenance — is a big draw for small and mid-sized manufacturers.

Conclusion

The affordability of Indian CNC machines manufacturer is not just a result of lower wages or cheaper materials — it’s a strategic outcome of efficient manufacturing, smart sourcing, and customer-focused innovation. As global demand for cost-effective, high-performance CNC machines continues to grow, Indian companies are well-positioned to lead the charge by combining affordability with quality and innovation.

0 notes

Text

North America Edge Computing Market Size, Share, Growth Factors, Competitive Landscape, with Regional Forecast (2022-2028)

The North America edge computing market is expected to grow from US$ 16,212.71 million in 2022 to US$ 52,976.45 million by 2028. It is estimated to grow at a CAGR of 21.8% from 2022 to 2028.

North America Edge Computing Market Introduction

Imagine a digital landscape where data processing occurs with minimal delay, bypassing the traditional route to distant cloud infrastructure. This is the essence of edge computing, a highly distributed network paradigm that strategically places computational power and data storage closer to the devices and applications that generate and consume data. By minimizing the distance data needs to travel, edge computing significantly reduces latency, enabling truly real-time responsiveness.

In today's interconnected world, the swift processing and transmission of data have become a fundamental requirement for business success. Numerous applications rely on minimal latency to enhance user experiences and improve customer satisfaction through faster and more seamless operation. Consider the smooth interactions in online meetings or the mission-critical computations in cloud-based systems where even fractions of a second can have significant consequences. Across diverse sectors such as healthcare, air traffic control, and critical defense scenarios, even incremental reductions in latency can accumulate into substantial improvements in overall network performance.

Download our Sample PDF Report

@ https://www.businessmarketinsights.com/sample/BMIRE00028905

North America Edge Computing Strategic Insights

To truly gain a competitive advantage in the North America Edge Computing market, a basic understanding is simply not enough. What's needed are insightful, data-driven strategic analyses that illuminate the complex dynamics of the industry, encompassing current trends, the influence of key players, and the unique characteristics of various regional sub-markets within North America.

These insights move beyond simple observation, offering concrete, actionable recommendations that empower organizations to differentiate themselves in a competitive marketplace. By identifying often-overlooked market segments or developing compelling and differentiated value propositions, businesses can establish a unique market identity. Leveraging the power of data analytics, these insights act as a compass, guiding industry participants – whether they are investors, manufacturers, or other stakeholders – in anticipating the subtle yet significant shifts within the market.

North America Edge Computing Market Segmentation

North America Edge Computing Market: By Component

Hardware

Software

Services

North America Edge Computing Market: By Application

Smart Cities

Industrial Internet of Things

Remote Monitoring

Content Delivery

Augmented Reality and Virtual Reality

North America Edge Computing Market: By Enterprise Size

SMEs and Large Enterprises

North America Edge Computing Market: By Verticals

Manufacturing

Energy and Utilities

Government

IT and Telecom

Retail and Consumer Goods

Transportation and Logistics

Healthcare

North America Edge Computing Market: Regions and Countries Covered

North America

US

Canada

Mexico

North America Edge Computing Market: Market leaders and key company profiles

ADLINK Technology Inc

Amazon Web Services

Dell Technologies

EdgeConnex Inc.

FogHorn Systems

Hewlett Packard Enterprise Development LP (HPE)

IBM Corporation

Litmus Automation, Inc

Microsoft Corporation

Vapor IO, Inc.

About Us:

Business Market Insights is a market research platform that provides subscription service for industry and company reports. Our research team has extensive professional expertise in domains such as Electronics & Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications

#North America Edge Computing Market#North America Edge Computing Market Size#North America Edge Computing Market Share

0 notes

Text

The Evolution of CAM (Computer-Aided Manufacturing) in Industry

Hello, engineering students and tech enthusiasts! If you’re curious about how products go from ideas to reality, let’s dive into the world of Computer-Aided Manufacturing (CAM). CAM has transformed industries, making manufacturing faster, smarter, and more precise. As your mentor, I’m excited to walk you through its evolution, from its early days to its role in today’s high-tech factories. With insights grounded in industry trends, this guide will show you why CAM is a game-changer for mechanical engineers.

The Birth of CAM: A New Era Begins

CAM started in the 1950s when computers first entered manufacturing. Early systems used punched tapes to control machines, a far cry from today’s tech. By the 1970s, Numerical Control (NC) machines evolved into Computer Numerical Control (CNC), allowing engineers to program tools with precision. A 2023 ASME report notes that these advancements cut production times by 40% in industries like aerospace. CAM was born to bridge design and production, turning digital models into physical parts with minimal human intervention.

The 1980s and 1990s: CAM Goes Mainstream

The 1980s brought CAD/CAM integration, letting engineers design and manufacture in one workflow. Software like Mastercam and CATIA emerged, enabling complex geometries for automotive and aviation parts. By the 1990s, CAM systems supported multi-axis machining, which meant machines could move in multiple directions for intricate shapes. According to a 2024 Manufacturing Technology Insights study, this boosted productivity by 25% in factories. If you’re at one of the best private engineering colleges in Odisha, like NM Institute of Engineering and Technology (NMIET), you’re likely using similar software in labs to simulate these processes, getting a taste of real-world applications.

The 2000s: Automation and Precision Take Over

The 2000s saw CAM embrace automation. Robotic arms, guided by CAM software, started handling repetitive tasks like welding and assembly. This was huge for industries like automotive, where companies like Toyota slashed production costs by 20%, per a 2023 Industry Week report. CAM also integrated with simulation tools, letting engineers test toolpaths virtually before cutting metal, reducing errors. Cloud-based CAM software, like Fusion 360, made collaboration easier, allowing teams to share designs globally. These tools are now standard in many engineering curriculums, giving students hands-on experience.

CAM Today: Industry 4.0 and Beyond

Fast forward to 2025, and CAM is at the heart of Industry 4.0. It’s now paired with AI, IoT, and additive manufacturing (3D printing). AI-powered CAM optimizes toolpaths, cutting waste by up to 15%, according to a 2024 McKinsey report. IoT connects machines to monitor performance in real-time, predicting maintenance needs. Additive manufacturing, guided by CAM, creates complex parts layer by layer, revolutionizing aerospace and medical device production. A 2024 Deloitte study predicts the global CAM market will reach $5.2 billion by 2030, driven by demand for smart manufacturing.

Students at the best private engineering colleges in Odisha are well-positioned to jump into this field. Institutes like NMIET, with modern labs and industry ties to companies like IBM, offer exposure to CNC machines and CAM software, helping you build skills employers value. The hands-on learning you get now is your ticket to thriving in this dynamic industry.

How to Prepare for a CAM Career

Want to be part of CAM’s future? Start with a strong grasp of mechanical engineering fundamentals like mechanics and materials science. Learn CAM software—Mastercam, Siemens NX, and Fusion 360 are industry favorites. A 2024 LinkedIn report found that 82% of CAM-related job postings list software proficiency as a must. Online courses on platforms like Coursera can help you master these tools.

Internships are key. Look for opportunities with manufacturers or CNC shops. A 2023 Glassdoor study showed that engineering interns with CAM experience are 30% more likely to land full-time roles. Network with professionals through ASME or LinkedIn, and attend industry events to stay updated on trends. Your college’s placement cell, especially at institutes like NMIET, might connect you with firms using CAM technologies.

Why CAM Matters for Your Future

CAM isn’t just about machines—it’s about innovation. It powers industries from automotive to healthcare, creating jobs for skilled engineers. Roles like CAM programmer or manufacturing engineer offer salaries ranging from ₹5-12 LPA in India, per 2024 Payscale data, with higher earnings as you gain experience. You could work for global giants like General Electric or local manufacturers, or even start your own CNC workshop.

Final Thoughts

The evolution of CAM has reshaped manufacturing, and it’s only getting bigger. From CNC machines to AI-driven factories, mechanical engineers are driving this revolution. Stay curious, master the tools, and seek hands-on experience. A 2024 Industry 4.0 report predicts a 25% rise in CAM-related jobs by 2030, so the opportunities are endless. Whether you’re at NMIET or another institute, use your education to dive into CAM. The future of manufacturing is in your hands—go shape it!

#best colleges in bhubaneswar#college of engineering bhubaneswar#best engineering colleges in orissa#best engineering colleges in bhubaneswar#best private engineering colleges in odisha#best engineering colleges in odisha

0 notes

Text

Unlocking Engineering Precision with FEA and CAD Integration

In today’s fast-paced and innovation-driven engineering environment, the ability to model, analyze, and validate designs before physical production is not just an advantage—it’s a necessity. This is where the integration of Computer-Aided Design (CAD) and Finite Element Analysis (FEA) becomes a game-changer. Together, these technologies provide engineers with the tools to optimize product designs, reduce development time, and minimize costs while ensuring product quality and reliability.

What is CAD?

Computer-Aided Design (CAD) refers to the use of computer software to create precise drawings, technical illustrations, and 3D models of products or parts. CAD software has become an indispensable tool in industries such as automotive, aerospace, electronics, and consumer goods, where design precision and visualization are critical.

CAD tools allow engineers and designers to:

Create 2D and 3D representations of products.

Modify and iterate designs with ease.

Visualize complex components before physical prototyping.

Integrate with manufacturing systems like CAM (Computer-Aided Manufacturing) for seamless production workflows.

What is FEA?

Finite Element Analysis (FEA) is a numerical method used to simulate and analyze physical phenomena such as structural stress, thermal performance, vibration, and fluid dynamics. By breaking down complex geometries into smaller, manageable elements (the "finite elements"), FEA allows for the detailed evaluation of how a product will perform under real-world conditions.

Engineers use FEA to:

Predict potential design failures before production.

Understand stress concentrations and material behavior.

Test various loading conditions and environmental factors.

Optimize designs for strength, weight, and performance.

The Power of CAD and FEA Integration

While CAD is primarily focused on designing the geometry and structure of a part or system, FEA provides insight into how that part will behave under various operational conditions. Integrating CAD and FEA creates a cohesive workflow that empowers engineers to design with performance in mind from the start.

Here are some key benefits of this integration:

1. Faster Design Cycles

The seamless flow of information from CAD models into FEA simulations eliminates the need to recreate geometry or manually input data. Design changes can be made in CAD and instantly updated in FEA, reducing time spent on repetitive tasks and speeding up design iterations.

2. Enhanced Design Accuracy

CAD models offer exact geometric representations, which are essential for reliable simulation in FEA. Using accurate CAD models in FEA ensures that the analysis reflects true product geometry, improving the validity of the results.

3. Cost Reduction

Identifying design flaws or inefficiencies early in the development cycle means fewer physical prototypes, less rework, and reduced material waste. This significantly lowers development costs and shortens time-to-market.

4. Optimized Performance

By using FEA within the CAD environment, engineers can simulate how designs respond to different forces and conditions. This allows for iterative optimization—adjusting shape, material, or thickness to achieve peak performance while minimizing weight and material usage.

5. Streamlined Collaboration

CAD/FEA integration fosters collaboration among engineering teams. Designers and analysts can work from a single model, share insights more effectively, and maintain version control throughout the product development process.

Real-World Applications

The CAD-FEA combination is transforming design processes across multiple industries:

Automotive: Simulating crash tests, heat dissipation in engines, and durability of suspension systems.

Aerospace: Ensuring structural integrity under extreme pressure and temperature conditions.

Medical Devices: Evaluating the strength and performance of implants and surgical tools.

Consumer Electronics: Assessing thermal performance of devices to prevent overheating.

Choosing the Right Tools

There are several CAD and FEA software platforms that offer strong integration, including:

SolidWorks + SolidWorks Simulation: A popular option for mechanical engineers, allowing integrated design and analysis.

Autodesk Inventor + Nastran: Offers a powerful suite for simulation and mechanical design.

PTC Creo + Creo Simulate: Known for high-fidelity simulation with real-time feedback during the design process.

Siemens NX: An advanced solution that tightly couples CAD and simulation for complex product development.

Best Practices for CAD/FEA Integration

Design for Analysis: When creating CAD models, think ahead to the FEA phase. Avoid overly complex geometry and ensure features like fillets and holes are appropriately represented.

Validate Mesh Quality: A proper mesh ensures simulation accuracy. Pay attention to mesh refinement in areas of high stress or geometric complexity.

Material Properties: Use accurate material data in your simulations. Many FEA tools include built-in libraries, but real-world testing or manufacturer data is often best.

Boundary Conditions: Realistic loading, constraints, and environmental conditions are key to getting valuable simulation results.

Iterative Process: Use FEA results to refine your CAD model. Small changes can lead to big improvements in performance and cost-efficiency.

The Future of CAD and FEA

As technologies like AI, machine learning, and cloud computing continue to evolve, CAD and FEA integration is becoming even more powerful. Generative design, where software automatically proposes optimal shapes based on performance requirements, is already pushing boundaries. Cloud-based platforms now allow for high-performance simulations without investing in expensive hardware.

Conclusion

The combination of CAD and FEA by Servotechinc empowers engineers to create better, smarter products in less time. By simulating real-world performance during the design phase, companies can deliver safer, more efficient, and more innovative solutions to market faster and more affordably.

Whether you're designing the next electric vehicle, a surgical implant, or a high-rise building component, integrating FEA into your CAD workflow gives you the insight and precision to engineer with confidence.

0 notes

Text

What are the key requirements for ISO 27017 Certification in the Netherlands?

ISO 27017 Certification in Netherlands , Cloud computing has become a foundation of trade operations in a time ruled by computerized change. Be that as it may, with expanded dependence on cloud situations comes the pressing requirement for vigorous security controls. This is where ISO 27017 Certification steps in: custom-made advertising rules, particularly for cloud-benefit suppliers and clients. Getting ISO 27017 Certification in the Netherlands illustrates a company’s commitment to cloud security and information protection.

Understanding ISO 27017 Certification in Netherlands

ISO/IEC 27017 is a universal standard that gives extra direction past ISO 27001 for executing cloud-specific security controls. It’s planned to diminish the hazard of security episodes in cloud situations and guarantee compliance with worldwide and Dutch information assurance laws.

Why ISO 27017 Things in the Netherlands

The Netherlands is a key player in the worldwide computerized economy, facilitating numerous information centers and tech ventures. With strict information assurance directions like the Common Information Security Direction (GDPR) input, Dutch organizations caring for touchy data in the cloud must guarantee the most elevated data security measures.

Key Necessities for ISO 27017 Certification in the Netherlands

Here are the essential prerequisites organizations must meet to get ISO 27017 Certification:

1. Compliance with ISO 27001

Before executing ISO 27017 controls, organizations must comply with ISO 27001, the pattern standard for data security administration frameworks (ISMS). ISO 27017 builds upon this establishment with cloud-specific controls.

2. Cloud-specific Security Controls

ISO 27017 presents 7 extra controls and gives direction on 37 existing ISO 27002 controls, including:

Responsibility Division: Clear parts between cloud benefit supplier and customer

Virtual Machine Arrangement: Secure sending and setup of virtual machines

Administrative Operations Assurance: Observing and confining to cloud-based authoritative activities

Cloud Benefit Assertions: Guaranteeing security obligations are tended to in SLAs

3. Information Area and Sovereignty

Organizations must know where their cloud information dwells. In the Netherlands, information sway is basic due to GDPR. ISO 27017 requires controls that characterize and confine information exchange over borders.

4. Third-party Cloud Supplier Management

Organizations must survey and oversee the dangers related to third-party cloud administrations. This incorporates assessing security hones, SLAs, and compliance with appropriate laws.

5. Occurrence Administration for Cloud Environments

ISO 27017 emphasizes strong cloud-specific occurrence reaction methods. Organizations must establish systems to efficiently distinguish, report, and resolve security breaches.

6. Secure Erasure of Cloud Data

Cloud benefit suppliers and clients must guarantee that information is hopelessly deleted when no longer required. This incorporates all reinforcements and repetitive information in shared cloud environments.

7. Straightforward Cloud Operations

Transparency concerning shared assets, multi-tenancy, and security obligations is fundamental. Organizations must build communication channels between clients and suppliers for chance and security updates.

Steps to Accomplish ISO 27017 Certification in the Netherlands

Conduct a thorough examination against ISO 27001 and ISO 27017 requirements

Develop and execute cloud-specific controls

Train staff and cloud clients on approaches and procedures

Conduct inner reviews to guarantee readiness

Undergo third-party certification review by a licensed body

Benefits of ISO 27017 Certification in the Netherlands

Enhanced belief with cloud clients and stakeholders

Better chance administration and cloud security governance

Competitive advantage in the cloud administration market

Compliance with Dutch and EU information assurance regulations

Reduced hazard of information breaches and cyberattacks

Why choose Factocert for ISO 27017 Certification in Malaysia?

We provide the best ISO 27017 certification consultants in Malaysia, who are very knowledgeable and provide you with the best solution. And to knowhow to get ISO 27017 certification in Malaysia Kindly reach us at [email protected]. ISO 27017 Certification consultants follow the guidelines set by the international organization for standardization and help the organization to implement ISO 27017 certification in Malaysia in an easy way with proper documentation and audit.

For more information visit: ISO 27017 Certification in Netherlands.

0 notes

Text

Demystifying the Stock Market: A Beginner’s Step-by-Step Guide

The stock market offers exciting opportunities for wealth creation. But for a beginner, navigating this complex world can seem daunting. This short guide will equip you with the essential steps and knowledge to confidently begin your stock trading journey.

Opening the Doors: Demat & Trading Accounts

Your first step is to establish two key accounts: a Demat account and a trading account. Think of your Demat account as a secure electronic vault to hold your purchased shares. The trading account acts as the interface to buy and sell these shares on the stock exchange. Reputable stockbrokers like Zerodha, Kotak Securities, or Angel Broking offer these accounts. Many brokers now have user-friendly mobile apps (like Zerodha Kite, Upstox Pro) that allow you to manage your Demat account and trade conveniently.

Understanding the Stock Market Landscape

India has two primary stock exchanges: the Bombay Stock Exchange (BSE) and the National Stock Exchange (NSE). Both exchanges list companies for trading. The NSE is the largest stock exchange in India by trading volume. When you invest through a broker, your trades are routed to one of these exchanges for execution.

Building Your Knowledge Arsenal

To make informed decisions, equip yourself with two crucial analysis methods:

Fundamental Analysis: This involves studying a company's financial health, its industry position, and overall market trends. Annual reports, news articles, and financial websites provide valuable resources for this analysis.

Technical Analysis: This focuses on historical price movements and chart patterns to predict future price trends. There are numerous online resources and courses available to learn technical analysis tools.

Discipline is Key: Risk Management Strategies

The stock market is inherently risky. Here are some strategies to mitigate risk:

Start Small: Begin with a small investment amount you can afford to lose. As your experience grows, you can gradually increase your investment capital.

Diversification: Don't put all your eggs in one basket. Spread your investments across different sectors and companies to minimize risk from any single company's performance.

Stop-Loss Orders: These pre-defined orders automatically sell your shares when the price falls below a certain level, helping you limit potential losses.

Learning Resources at Your Fingertips

The Securities and Exchange Board of India (SEBI) offers a vast repository of investor education resources on their website. Additionally, many stockbrokers provide educational materials and webinars for beginners. Consider starting with these resources before diving deeper into technical analysis courses.

Poddar Business School, a top B-school in Jaipur features PGDM and MBA programs with specializations in human resources, marketing, finance, operation, entrepreneurship and start-up technologies, etc.

Trading Platforms and Apps

Gone are the days of needing a desktop computer to trade. Today, several user-friendly mobile apps and online trading platforms allow you to trade conveniently from your phone or computer. Here are some popular options:

Zerodha Kite: Known for its user-friendly interface and robust features, Zerodha Kite is a popular choice for beginners and experienced traders alike.

Upstox Pro: This app caters to traders who prioritize advanced charting tools and technical analysis features for active trading.

Paytm Money: This app offers a user-friendly interface and integrates seamlessly with the Paytm ecosystem, making it convenient for those already familiar with the Paytm platform.

Angel One: This platform provides a comprehensive suite of investment options, research tools, and educational resources, making it a good choice for those who want a one-stop shop for their investment needs.

Mutual Funds vs. Stock Trading

While both offer opportunities for growth, there are key differences:

Control: In stock trading, you directly choose and buy individual stocks. With mutual funds, a fund manager makes investment decisions for you, spreading your money across various holdings.

Time Commitment: Stock trading requires active research and monitoring. Mutual funds offer a more passive approach, with the fund manager handling the heavy lifting.

Diversification: Stock trading requires effort to build a diversified portfolio. Mutual funds inherently offer diversification due to their multi-holding nature.

Choose what suits your investment style and risk tolerance!

Remember: The stock market is a marathon, not a sprint. Be patient, prioritize learning, and develop a sound investment strategy. Most importantly, never invest money you can't afford to lose. With discipline and continuous learning, you can navigate the stock market with confidence and potentially build a strong financial future.

0 notes

Text

#Computer Numerical Control Market#Computer Numerical Control Market Share#Computer Numerical Control Market Size#Computer Numerical Control Market Research#Computer Numerical Control Industry#What is Computer Numerical Control?

0 notes

Text

Risks and Rewards: Navigating the Evolving Speech-to-Text API Market

Speech-to-text API Market Growth & Trends

The global speech-to-text API market is experiencing robust growth, projected to reach USD 8,569.5 million by 2030, growing at a CAGR of 14.1% from 2025 to 2030. This expansion is driven by several key factors:

Rising Popularity of Smart Speakers and Smart Mobile Phones:

The widespread adoption of voice-enabled systems in smart speakers and mobile phones is a significant driver. These devices leverage augmented reality (AR), machine learning (ML), and natural language processing (NLP) to automate conversations and provide a hands-free user experience. As more consumers integrate these devices into their daily routines, the demand for underlying speech-to-text API solutions continues to surge.

Increasing Demand for Transcription and Real-time Support Services:

The growing need for accurate transcription and real-time support services across various industries is motivating industry giants to develop advanced speech-to-text API solutions. This includes applications in contact centers, legal documentation, content creation, and more, where converting spoken words into text efficiently is crucial.

Growth in Virtual/Digital Conferences and Events:

The increasing number of virtual and digital conferences and events hosted by technology giants and other enterprises is boosting the demand for speech-to-text solutions. These solutions offer low cost, high accuracy, and faster transcription, enabling seamless communication and accessibility for a global audience. For instance, events like PegaWorldiNspire utilize AI technologies, including speech-to-text, to enhance the viewer experience.

Advancements in Artificial Intelligence (AI) and Cloud-based Services:

Significant advancements in AI, particularly in machine learning and natural language processing, are enhancing the accuracy and capabilities of speech-to-text APIs. The rising popularity of cloud-based services also facilitates the adoption of these solutions by offering scalability, cost-efficiency, and remote accessibility.

Enhanced Accessibility for People with Disabilities:

Speech-to-text solutions play a vital role in improving accessibility for individuals with disabilities. They allow people with visual impairments to "hear" written words when combined with screen readers and provide voice control for individuals with motor impairments. Companies like Voiceitt are specifically developing speech recognition for non-standard speech, opening up voice technology for people with speech disabilities.

Continuous Product Improvement and Innovation:

Companies in the market are actively improving their product ranges by integrating advanced technologies. For example, Google LLC launched a new model for its Speech-to-Text API in April 2022, improving accuracy across numerous languages and supporting diverse acoustic and environmental conditions. Similarly, IBM Corporation upgraded its speech-to-text recognition service in March 2020, enhancing tracking capabilities and adding speaker labels for Korean and German language models. Other key players like Amazon Transcribe, Microsoft Azure Speech Service, Nuance (Dragon Speech Recognition), Deepgram, and AssemblyAI are continuously innovating to offer higher accuracy, multilingual support, and industry-specific solutions.

Curious about the Speech-to-text API Market? Download your FREE sample copy now and get a sneak peek into the latest insights and trends.

Speech-to-text API Market Report Highlights

Software component led the market with a revenue share of 70.3% in 2024. High penetration of software segment can be attributed to advancements in increased computing power, information storage capacity, and parallel processing capabilities to supply high-end services.

The on-premises segment dominates the market with a revenue share in 2024. The on-premises deployment model is preferred by sectors related to communication, marketing, HR, legal departments, studios, researchers, and broadcasters, among others, due to security concerns.

The large enterprise segment dominates the market, with a revenue share in 2024. The major factor propelling the growth of the segment is the high capital stability, which allows large enterprises to afford such APIs integrations.

The fraud detection & prevention segment dominates the market with a revenue share in 2024. This is due to the growing need for speech-to-text APIs in the entertainment and media industry.

The BFSI segment dominates the market, with a revenue share in 2024. The major factor propelling segment growth is using speech-to-text converters to analyze the customer’s feedback.

Speech-to-text API Market Segmentation

Grand View Research has segmented the global Speech-to-text API market based on components, deployment, organization size, application, verticals, and region:

Speech-to-text API Component Outlook (Revenue, USD Million, 2018 - 2030)

Software

Service

Speech-to-text API Deployment Outlook (Revenue, USD Million, 2018 - 2030)

On-premises

Cloud

Speech-to-text API Organization size Outlook (Revenue, USD Million, 2018 - 2030)

Large Enterprises

Small & Medium-sized Enterprises (SMEs)

Speech-to-text API Application Outlook (Revenue, USD Million, 2018 - 2030)

Contact center and customer management

Content Transcription

Fraud Detection and Prevention

Risk and Compliance Management

Subtitle Generation

Others

Speech-to-text API Verticals Outlook (Revenue, USD Million, 2018 - 2030)

BFSI

IT & Telecom

Healthcare

Retail & eCommerce

Government & Defense

Media & Entertainment

Travel & Hospitality

Others

Download your FREE sample PDF copy of the Speech-to-text API Market today and explore key data and trends.

0 notes

Text

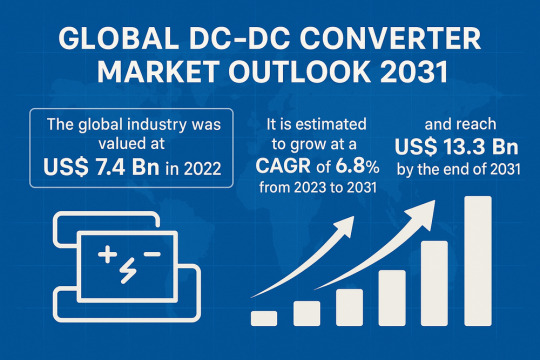

Technological Innovation Catalyzes Growth in the DC-DC Converter Market

The Global DC-DC Converter Market Outlook 2031 report reveals that the market, valued at USD 7.4 billion in 2022, is projected to expand at a CAGR of 6.8% from 2023 through 2031, reaching USD 13.3 billion by the end of 2031.

Market Overview: DC-DC converters are essential for managing power distribution across myriad electronic systems, converting input DC voltages to regulated outputs with high efficiency and minimal noise. From automotive and telecommunications to aerospace and renewable energy, these converters ensure optimal performance and reliability. In 2022, the global DC-DC converter market was valued at USD 7.4 billion. With surging demand for energy-efficient electronics and rapid electrification of transportation, the market is on track to achieve USD 13.3 billion by 2031, growing at a steady 6.8% CAGR.

Market Drivers & Trends

Energy Efficiency Imperative: As industries pursue greener operations and lower operating costs, high-efficiency DC-DC converters reduce energy losses and extend battery life in portable and off‑grid applications.

Electric Vehicle (EV) Adoption: Rising EV sales necessitate reliable DC-DC converters to step down high‑voltage battery output for auxiliary loads such as lighting, infotainment, and safety systems.

Technological Advancements: Innovations in wide‑bandgap semiconductors (e.g., SiC, GaN), digital control algorithms, and higher power density architectures are driving performance improvements and miniaturization.

Power Density & Integration: The trend toward compact, integrated power modules that combine control, protection, and conversion functions is reshaping customer expectations and creating new design opportunities.

Key Players and Industry Leaders

The global DC-DC converter landscape is highly fragmented, with numerous specialized and diversified vendors competing on quality, innovation, and customization:

ABB Ltd.

Advanced Energy Industries, Inc.

Bel Fuse Inc.

Delta Electronics, Inc.

FDK Corporation

FLEX Ltd.

Infineon Technologies AG

MEAN WELL Enterprises Co., Ltd.

Meggitt PLC

Murata Manufacturing Co., Ltd.

STMicroelectronics N.V.

TDK Corporation

Texas Instruments Incorporated

Vicor Corporation

XP Power

Other Key Players

Each company’s profile in the report includes an overview, financial performance, R&D focus, product portfolio, and strategic initiatives.

Download to explore critical insights from our Report in this sample - https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=57555

Recent Developments

October 2023: Bel Fuse launched the 700DNG40-24-8, a liquid‑cooled 4 kW DC-DC converter for EV and HEV auxiliary systems.

September 2023: FLEX Ltd. introduced the 300 W PKU4317D series for telecom/datacom applications, featuring comprehensive protection against over-temperature, under-voltage, and short circuits.

March 2023: Bel Fuse rolled out the RDT-6Y series for railway applications, offering a 12:1 input range (14–160 VDC).

November 2021: Eaton eMobility secured a contract for a 24 V-to-12 V DC-DC converter in heavy‑duty battery-electric vehicles, emphasizing noise reduction and interference rejection.

November 2019: Delta Electronics debuted its B70SP series (500 W, 91.5% efficiency) for industrial and off-road electric vehicles.

Latest Market Trends

Isolated Converters Dominate: In 2022, isolated DC-DC converters commanded a 73.1% share, driven by safety isolation, noise suppression, and ground‑potential flexibility. This segment is forecast to grow at 6.2% CAGR through 2031.

Data Center Electrification: With the explosion of high‑performance computing, data center racks increasingly rely on dense DC-DC modules to manage power in space-constrained environments. The data center segment held an 18.5% share in 2022.

Modular, Scalable Architectures: Vendors are offering plug-and-play power blocks that can be paralleled or stacked to meet variable load demands, enhancing scalability and reducing development time.

Market Opportunities

Renewable Energy Integration: As solar and wind installations proliferate, DC microgrids and battery storage systems require efficient converters to balance generation, storage, and consumption.

5G & Edge Computing: Telecom base stations and edge data nodes demand high-reliability, compact converters to support continuous operation in diverse environments.

Industrial Automation & IIoT: Smart factories and robotics applications benefit from precision power control, enabling predictive maintenance and higher uptime.

Future Outlook

Analysts anticipate sustained expansion of the DC-DC converter market, underpinned by global electrification trends and stringent energy regulations. Innovation in digital control and AI‑driven power management is set to unlock further efficiency gains. By 2031, next‑generation converters will support higher voltage battery systems (>800 V), bidirectional power flow for vehicle‑to-grid (V2G) applications, and advanced fault‑tolerance features for critical infrastructure.

Market Segmentation

By Type

Isolated DC-DC Converter

Non‑isolated DC-DC Converter

By Power Range

Up to 100 W; 100–500 W; 500–1 000 W; 1 000–1 500 W; 1 500–2 000 W; Above 2 000 W

By Input Voltage

Up to 20 V; 20–40 V; 40–60 V; 60–100 V; Above 100 V

By Output Voltage

Up to 12 V; 12–24 V; 24–48 V; 48–72 V; 72–100 V; Above 100 V

By Brick Size

1/2, 1/4, 1/8, 1/16, 1/32 Brick; Full Brick

By Mounting

Chassis, Through‑Hole, SMD/SMT, DIN Rail, Others

By Application

Data Centers, Industrial Automation, Automotive, Aircraft/Spacecraft, Smartphones, Home Appliances, Computing Devices, Solar Inverters, Others

By End‑use Industry

Automotive & Transportation, Aerospace & Defense, Electronics & Semiconductor, IT & Telecom, Industrial, Energy & Utility, Others

By Region

North America, Europe, Asia Pacific, Latin America, Middle East & Africa

Why Buy This Report?

Comprehensive Analysis: Global and regional market sizing, historical data (2017–2021), and detailed forecasts (2023–2031).

Multi-layered Segmentation: Cross-segment insights by type, power range, voltage, mounting, application, and end‑use.

Competitive Landscape: In-depth profiles of 15+ key players, market share analysis, strategic initiatives, and recent developments.

Strategic Tools: Porter’s Five Forces, value chain analysis, and trend mapping to guide investment and product development.

Rich Data Package: Electronic report (PDF) plus Excel database for customized analysis.

About Transparency Market Research Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information. Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports. Contact: Transparency Market Research Inc. CORPORATE HEADQUARTER DOWNTOWN, 1000 N. West Street, Suite 1200, Wilmington, Delaware 19801 USA Tel: +1-518-618-1030 USA - Canada Toll Free: 866-552-3453 Website: https://www.transparencymarketresearch.com Email: [email protected]

0 notes

Text

An In-Depth Look at the Growth of U.S. Commercial Duct Smoke Detector Market

The U.S. commercial duct smoke detector market size is estimated to reach USD 226.0 million by 2030, registering to grow at a CAGR of 5.0% from 2025 to 2030 according to a new report by Grand View Research, Inc. Construction activities in the commercial sector are rising with the growing demand for living spaces, offices, hospitals, shopping malls, and business centers, among others. Increased construction spending due to economic & industrial development and rapid population growth is expected to boost the demand for commercial duct smoke detectors over the forecast period. Various emerging countries have made significant investments in public infrastructure such as hospitals, and offices on account of the increasing population and rapid industrialization.

Duct smoke detectors can be used to control ventilation dampers in some situations. They are also utilized to safeguard HVAC systems from smoke and fire damage. These detectors are also used in equipment protection applications, such as the ventilation/exhaust ductworks of computers and tape drives. The rise in the usage of duct smoke detectors is anticipated to fuel the growth of the commercial duct smoke detectors industry in U.S. in the coming years.

Duct smoke detectors are specially designed for installation in HVAC ducts to identify the smoke circulating through HVAC systems. They are deployed in buildings to avoid panic, injury, and property damage during emergencies, as well as for notifying users that smoke is passing through HVAC ducts. They also raise alarms about the closing down of air handlers and fans to prevent smoke from circulating within buildings. These detectors can also be set to solely turn off the supply fans of buildings without impacting the operations of return fans. In several situations, this procedure is adopted since it aids in the removal of smoke and other impurities, created in the air by the fire.

Manufacturers in the U.S. commercial duct smoke detectors industry adopt numerous strategies, including joint ventures, mergers, acquisitions, geographical expansions, and new product developments to augment their market adoption. Furthermore, they also cater to the shifting technological demand for equipment from various end-use industries such as commercial. For instance, in August 2021, the 910 series fire alarm control panel was announced by National Time & Signal. This sturdy and adaptable panel offers integrated LAN and mobile calling as well as the top constant-voltage notification outputs available in the market.

Request Free Sample PDF of U.S. Commercial Duct Smoke Detector Market Size, Share & Trends Analysis Report

U.S. Commercial Duct Smoke Detector Market Report Highlights

• The ionization duct smoke detector segment accounted for 25.0% market share due to their sensitivity to fast-burning fires, which are typically associated with the rapid spread of flames in commercial spaces.